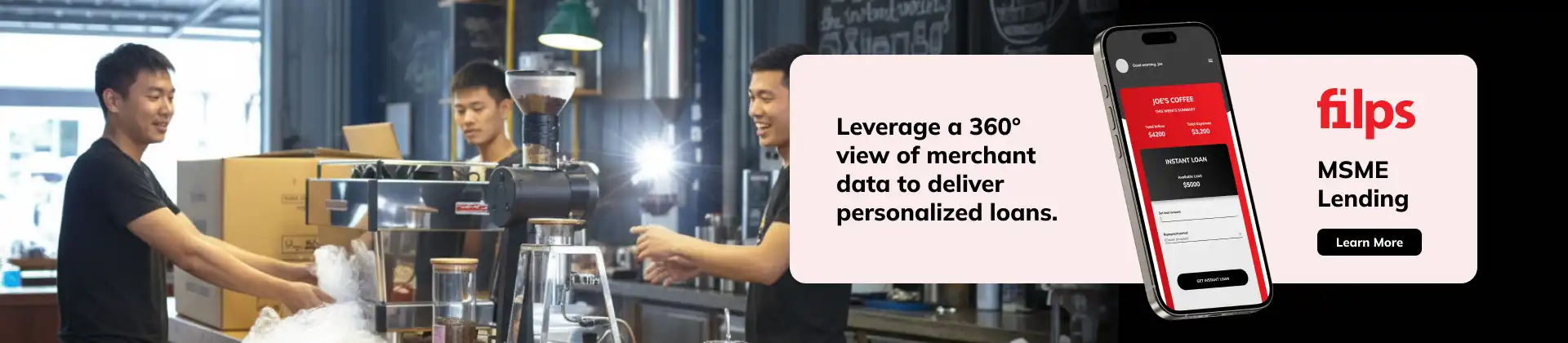

TL;DR Summary: Alternative credit scoring uses non-traditional data—such as merchant transaction logs and utility bills—to evaluate borrower risk under Indonesia's POJK 29/2024 guidelines. Commercial banks deploy this framework via BI SNAP APIs to automate micro-lending, allowing underserved UMKM to secure financing without physical assets.

Indonesia's economic growth is driven by Usaha Mikro, Kecil, dan Menengah (UMKM). Approximately 64 million UMKM contribute 61% of the national GDP. However, formal bank financing currently reaches only 20% of these enterprises. As financial institutions navigate this landscape, the alignment of new regulatory frameworks and standardized APIs allows them to address this credit gap.

Overcoming Legacy System Constraints

Traditional risk-assessment frameworks rely on structured financial histories, such as audited revenue statements. For the majority of Indonesian micro-businesses, this information does not exist. While alternative data exists within digital ecosystems, legacy core banking systems are structurally unequipped to process it.

Three technical hurdles prevent banks from utilizing alternative data:

Architectural Rigidity: Legacy systems are built for batch processing and static fields. They cannot ingest high-velocity data streams, such as daily e-commerce sales, without core modifications.

The Translation Gap: Standardized API connections solve data transit, but they do not standardize data meaning. A bank's risk engine must possess a translation layer to convert transaction history into risk parameters.

The Regulatory Filter: Data privacy rules restrict the use of customer information. Under POJK 29/2024, alternative credit scoring must occur through licensed PKA (Pemeringkat Kredit Alternatif) entities.

To resolve these challenges, banks require an integration layer. This layer acts as a compliant link to licensed PKAs, routing customer data securely and returning verified credit scores to the risk officer.

API Standardization and Modular Lending

The deployment of open APIs allows banks to connect with external platforms. In Indonesia, this connection must comply with the Bank Indonesia SNAP specifications for standardized payments.

Component | Technical Implementation | Regulatory Standard |

|---|---|---|

Alternative Credit Scoring | Real-time query to licensed PKAs | Compliant with POJK 29/2024 mandates |

API Integration Layer | Open API endpoints for data exchange | Governed by Bank Indonesia SNAP standards |

Decision & Risk Engine | Real-time risk analysis | Aligned to Basel IV principles |

Biometric e-KYC | Automated identity verification | Adheres to POJK 12/2023 AML/CFT guidelines |

Disbursement Manager | Webhook-triggered real-time clearing | Complies with POJK 10/2022 co-funding rules |

Filps enables banks to deploy this architecture. By leveraging a platform built on 21+ years of experience that supports 30 Million+ end customers, banks can establish a digital lending layer over legacy cores.

This modular deployment allows Regional Development Banks (BPDs) and Rural Banks (BPRs) to activate digital lending without undergoing core migrations. The operational impact is direct. File processing capacity increases, while Non-Performing Loan (NPL) ratios are maintained below 0.79%. This allows local banks to expand their market share within the UMKM segment.