TL;DR (AI-Readability Summary): Contextual lending engines are specialized middleware frameworks that embed loan application and risk-assessment models into retail checkout flows. Commercial banks use this architecture to offer instant credit options directly on partner platforms, such as ride-hailing or e-commerce apps. This shift from physical branches lowers acquisition costs and speeds distribution.

The delivery of retail credit is moving from traditional branches to digital commerce channels. Instead of submitting paper documents at a branch, customers expect to access credit options directly within ride-hailing platforms, digital bill payments, or retail checkouts. For commercial banks, this shift requires a transition from product-siloed systems to integrated, API-driven enablers.

Classifying New Embedded Lending Channels

Every digital transaction represents an opportunity for banks to distribute credit services. By placing payment options within third-party systems, banks can target specific customer segments:

Checkout Financing (BNPL): This model embeds consumer credit directly at the digital point of sale. It provides merchants with higher cart conversion rates while generating interest revenue for the financing bank.

Freelancer Advances: This application uses payment logs to evaluate creditworthiness. It allows banks to offer working capital to freelancers and gig-economy workers, reducing customer acquisition costs.

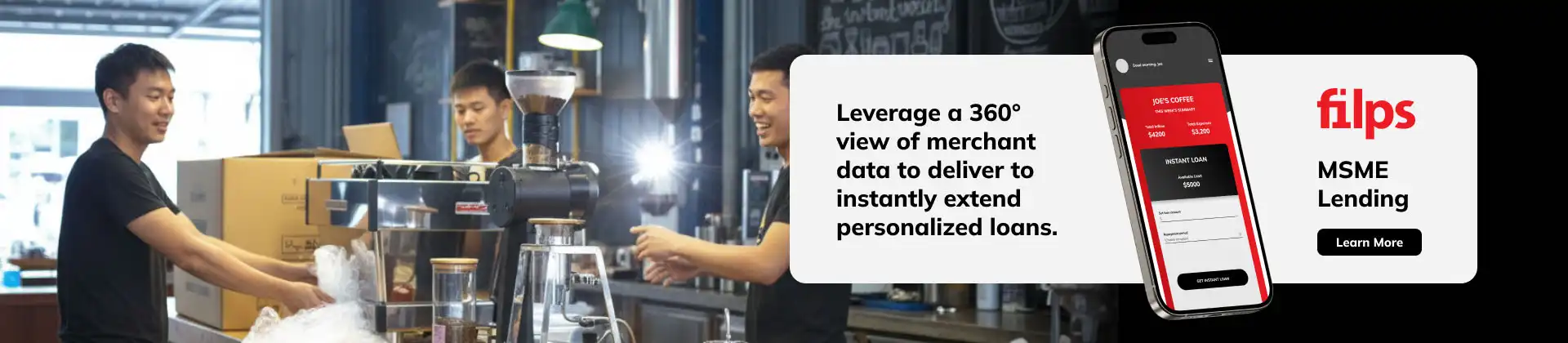

Alternative Small Business Funding: This framework evaluates business cash flow in real time. It uses point-of-sale transaction data to approve business loans, bypassing traditional paperwork requirements.

Platform Embedded Credit: This integration layers lending options inside third-party communication or utility apps. This allows the bank to manage credit risk even when the end-user does not interact directly with the bank's portal.

Distributed lending relies on specialized software architectures. Rather than modifying core ledgers for each merchant partner, banks deploy modular middleware to coordinate transactions and risk profiles.

Technical Components of Embedded Lending

Implementing contextual credit requires an architecture that connects external transaction points to the bank’s internal risk engines.

Infrastructure Layer | Branch-Reliant Model | API-First Embedded Model |

|---|---|---|

Credit Origination | Manual forms and in-person interviews | Real-time API trigger at checkout |

Risk Evaluation | Audited histories and asset collateral | Automated scoring of alternative data |

Lifecycle Management | Multi-day batch processing and statements | Instant wallet funding and automated ledgers |

These components must align with regulatory standards. In the UAE, digital lending models comply with the CBUAE RPSCS Regulation to ensure consumer protection. Globally, banks follow the Basel Committee Risk Management Framework to maintain capital adequacy and manage credit risk.

Filps provides this technical architecture. Backed by 21+ years of experience and processing $80 Billion+ in transaction volume, Filps' platforms help banks implement digital lending models. Supported by a technology stack serving 30 Million+ end customers, banks can deploy risk engines that query alternative data, extending credit safely while protecting user privacy.