TL;DR: Real-time payment security requires shifting from post-transaction disputes to proactive, network-edge risk scoring. This article explains:

How to block ATO and CNP fraud through real-time session and card checkout monitoring.

How to achieve sub-10ms evaluations using parallel metadata scoring to prevent checkout friction.

How to streamline RiskOps using maker-checker workflows for regulator-ready audit trails.

The Real-Time Fraud Dilemma

Commercial banks operate on a thin margin of customer trust. This is only intensified with the growth of instant clearing networks. The acceleration of real-time account-to-account (A2A) transfers has removed the lead times that previously gave security teams a window to intercept suspicious transactions. Because transfers now settle in seconds, prevention must happen at the moment of authorization.

Fraudsters have quickly adapted by automating their attacks, exploiting the gap between transaction speed and security response times. Traditional rule-based engines, which generally rely on rigid IF-THEN parameters, fail to keep pace with these automated tactics because attackers can easily bypass static thresholds by slightly adjusting their behavioral patterns. This constant adaptation leaves risk teams trapped in a reactive cycle, driving up operational overhead.

Anatomy of Modern Channel Vulnerability

Securing digital banking channels requires a precise, defense-in-depth approach against two primary threats: Account Takeover (ATO) and Card-Not-Present (CNP) fraud.

Account Takeover (ATO)

Account Takeover has evolved from basic phishing into industrialized credential stuffing. According to the SEON credential stuffing report, credential stuffing accounts for approximately 34% of all account entry points. Fraudsters deploy automated botnets to test leaked credentials across multiple banking portals simultaneously, easily bypassing legacy security barriers. Traditional authentication mechanisms like static passwords and SMS-based verification are no longer sufficient to stop these automated entries.

Once entry is gained, attackers typically execute session hijacking rather than immediate withdrawals. They capture active session tokens to bypass multi-factor authentication checkpoints, quietly monitoring transaction histories and limits. They wait for a low-activity window—often late-night hours—to drain the account. Defending against this vector requires continuous, silent behavioral profiling that monitors device indicators, mouse telemetry, and typing biometrics throughout the active session.

Card-Not-Present (CNP) Fraud

Card-Not-Present fraud remains a persistent risk for card issuers. Sourced to the Nilson Report card fraud trends, global card fraud losses are projected to reach $43 billion by 2026, heavily driven by the rise of mobile commerce. Mobile wallets now represent over half of global online commerce spend, making them a primary target for credential theft.

To mitigate CNP fraud without degrading cardholder checkout experience, banks must evaluate risk prior to authorization. Traditional card protection relies on retrospective chargeback disputes, which only trigger after the fraud has occurred. Applying blanket blocks at the merchant gateway reduces fraud but introduces high transaction friction, leading to false declines. Dynamic, pre-authorization risk scoring resolves this dilemma by analyzing transaction metadata in real-time, verifying user legitimacy without impacting transaction completion.

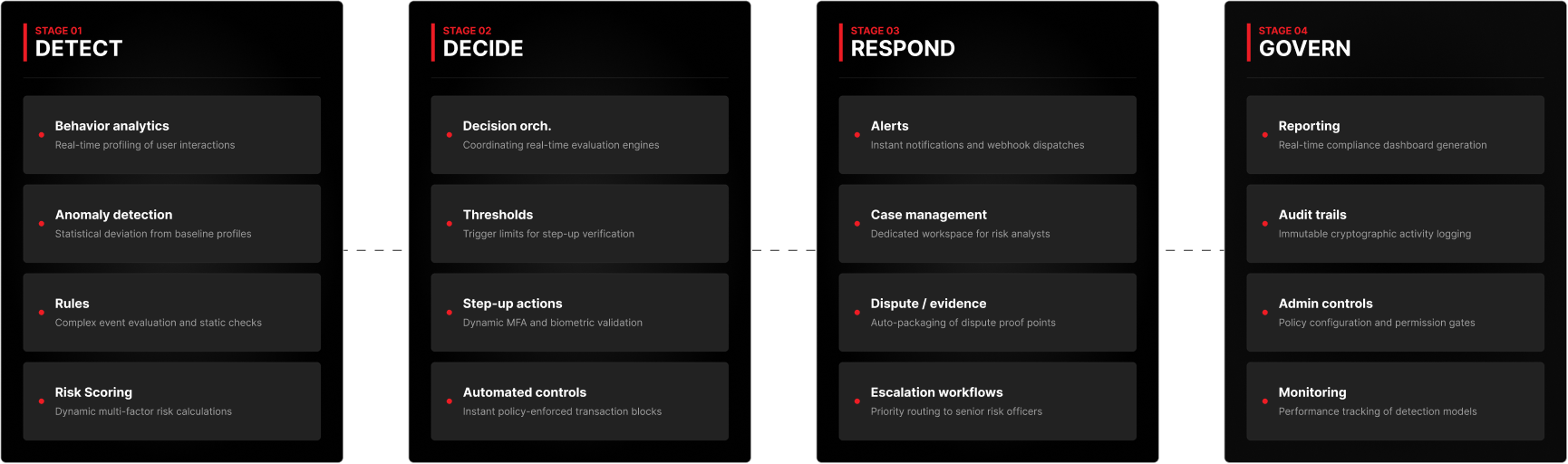

Unified Defense: ChannelGuard, CardGuard, and PaymentTrust

Defending against multi-vector fraud requires a modular control layer rather than a single monolithic platform. flxShield operates on this principle, isolating and protecting distinct transaction routes through interoperable modules. This modular structure allows banks to deploy targeted security layers where they are needed most.

The platform orchestrates fraud mitigation through four operational stages:

ChannelGuard protects the session and device layers by analyzing device fingerprints and user interaction biometrics at login, blocking automated botnets before they enter the banking interface.

CardGuard secures the card lifecycle, analyzing incoming physical and CNP transactions in real-time to flag velocity attacks, merchant risk, and geographical anomalies.

PaymentTrust monitors account-to-account transfers, evaluating transaction velocity and beneficiary account risk within mobile banking channels to block authorized push payment (APP) scams.

Security Module | Target Attack Vectors | Technical Mechanism | Operational Benefit |

|---|---|---|---|

ChannelGuard | Account Takeover (ATO), Session Hijacking, Botnets | Continuous device profiling, behavioral biometrics, network route analysis | Blocks unauthorized access before transaction initialization. |

CardGuard | Card-Not-Present (CNP) Fraud, Card Cloning, Identity Theft | Real-time authorization analysis, merchant risk evaluation | Reductions in card fraud losses without increasing checkout friction. |

PaymentTrust | Authorized Push Payment (APP) Scams, Money Mule Transfers | Velocity monitoring, destination account profiling, anomaly detection | Intercepts high-risk transfers before settlement clears. |

Operational Case Management with flxShield's RiskOps Module

Deploying advanced detection modules is only effective if analysts can respond to alerts quickly. When internal operations are fragmented, risk teams struggle under high alert volumes and disconnected workspaces. This operational drag delays dispute resolution and exposes the bank to regulatory penalties.

Establishing a unified case management framework through flxShield’s RiskOps module resolves these operational bottlenecks. The RiskOps module consolidates alerts from ChannelGuard, CardGuard, and PaymentTrust, giving analysts a single interface to review case histories. Instead of pivoting between multiple screens to trace a customer's device profile and card transaction history, risk officers access a unified timeline. This consolidated view reduces average handling times, allowing analysts to resolve alerts before transactions clear.

Strong governance is built into this workflow through maker-checker authorization protocols. When an analyst identifies a high-risk account, any request to freeze funds or block access must be approved by a secondary supervisor. This structured validation prevents unauthorized actions and reduces the risk of internal abuse. Implementing maker-checker workflows within dispute management operations ensures strict compliance. All operational decisions—from initial alert generation to final resolution—are logged in a compliance-ready audit trail. This clear record simplifies regulatory reporting and provides the board with verifiable metrics on the bank's risk posture.

Why Data Sovereignty Demands Hybrid Architectures

Operating in emerging financial markets requires compliance with strict data residency laws. Many central banks mandate that transactional logs and customer records remain within national borders, a requirement that cloud-only security tools cannot fulfill. Selecting a deployment model that supports local data residency is critical for banks to remain compliant.

To navigate this constraint, banks require deployment flexibility. Security architectures must be compatible with on-prem deployment, private cloud, or hybrid models. Storing sensitive customer data within the bank's physical datacenter allows the institution to retain complete sovereignty over its infrastructure. The system processes transaction metadata locally, complying with regulatory mandates like the CBUAE retail payment regulations while delivering sub-second latency for risk evaluations. A secure local deployment ensures that fraud scoring latency remains below 10 milliseconds.

This local infrastructure also protects the bank from external network disruptions. If international connectivity is lost, the local fraud detection engine continues to operate without interruption, ensuring uninterrupted security. This local resilience is essential for maintaining systemic stability, securing transaction streams even during major network outages.

Designing a Phased Integration Path

Upgrading fraud prevention does not require a costly, high-risk core banking overhaul. Financial institutions can adopt a phased integration strategy. By deploying modular components—starting with the most vulnerable channel—banks can secure critical vectors immediately.

Phase 1 Deploy session-level controls to secure mobile logins and block automated botnets.

Phase 2 Integrate account-based velocity checks to monitor instant transfers and intercept mule activity.

Phase 3 Activate real-time card authorization monitoring to protect CNP transactions.

This progressive integration minimizes deployment risk, allowing banks to modernize their security posture without interrupting daily banking operations. To support this phased, hybrid deployment model, Filps provides flxShield. The platform is built from our global experience enabling digital banking channels across 60+ partner BFIs, managing security for 30 Million+ end customers served and 1M+ merchants with over $80 Billion+ in transaction volume, backed by 21+ Years of fintech experience. Select an on-premise deployment or hybrid layout to align with regional guidelines.

About the author

Rhishikesh (Rishi) Nepal brings nearly a decade of experience at the intersection of fintech, digital banking, product innovation, and strategic partnerships. He has led the development and commercialization of data-driven financial solutions, helping financial institutions leverage AI, analytics, and digital technologies to improve lending, risk management, customer engagement, and operational efficiency.

His expertise spans product management, business strategy, partnership development, and digital transformation and has driven the launch and growth of numerous banking and fintech products used by leading financial institutions.

With a background in AI-powered lending, credit scoring, customer analytics, and financial technology innovation, he is passionate about building meaningful collaborations that accelerate digital adoption and create sustainable value for businesses and customers alike.