QUICK TAKE: Shared risk operations is a collaborative security model where a central payment switch runs real-time fraud monitoring as a shared service. This article outlines:

Systemic rail protection by blocking clearing-vector exploits at the network boundary.

Zero-latency routing by scoring transaction metadata in parallel with payment payloads.

Multi-tenant RiskOps dashboards that segregate member alerts while aggregating threat intelligence.

The Operational Shift of Real-Time Clearing

The transition to instant payment networks has changed the operational scale and risk profile of national clearing systems. As documented in the ACI Worldwide Prime Time for Real-Time Report, global instant payment volumes continue to experience compound growth, forcing clearing systems to modernize. Historically, central switches were designed to route message payloads and log transactions for batch settlement, leaving risk management to individual member banks. However, when settlement becomes immediate and irreversible, this traditional division of labor creates an operational gap. Controls that once relied on post-transaction batch clearing can no longer intercept high-velocity fraud before funds leave the network.

As instant payment schemes scale, the elimination of clearing delays collapses the window available to detect and intercept fraudulent transaction flows. Settlement is now irreversible. Data from the UK Finance Fraud Report highlights that authorized push payment (APP) fraud and coordinated money-mule schemes have escalated as transactions clear in seconds. To evade detection, attackers exploit this speed, splitting a large illicit payload into low-value transfers and distributing them across multiple recipient banks simultaneously. Because local fraud systems analyze incoming transactions in isolation, a single $1,000 transfer appears normal to a member bank's risk engine. The systemic pattern—the "fan-out" velocity profile of fifty matching transactions clearing across ten member banks within a three-minute window—remains invisible unless analyzed at the central switch intersection.

To close this gap, switches are shifting from basic transaction routing to running real-time risk evaluation directly at the network level. Because the switch sits at the intersection of all clearing paths, it is the only point in the network that can analyze traffic patterns across all member institutions. From this vantage point, the switch can flag anomalies before they propagate through the wider clearing network.

The Switch Security Challenge: Real-Time vs. Latency

Enforcing real-time security checks at the network boundary introduces a primary technical challenge, specifically processing latency. Core switches operate with a total transit budget of under two milliseconds per message, frequently handling peak loads exceeding 5,000 transactions per second. Traditional fraud engines require synchronous database lookups or blocking REST API queries, which introduce 50 to 100 milliseconds of latency. Under peak transaction volume, this latency creates queue backpressure in the message buffer, triggering socket timeouts and network-wide clearing failures.

Modern trust infrastructure resolves this speed issue through parallel metadata evaluation. As the transaction enters the switch, a duplicate of the transaction metadata is streamed to a parallel risk engine. While the core switch performs standard message validation and routing path lookups, the risk engine scores the transaction in under ten milliseconds. This risk score is then merged back into the outbound message payload using standardized supplementary data blocks defined by ISO 20022 messaging standards before the switch transmits the request to the receiving bank. This in-flight enrichment occurs within the standard messaging window, enabling the receiving bank to block or hold the funds using standard message fields without delaying core network throughput.

Unified Switch Defense: Deploying Modular Trust Rails

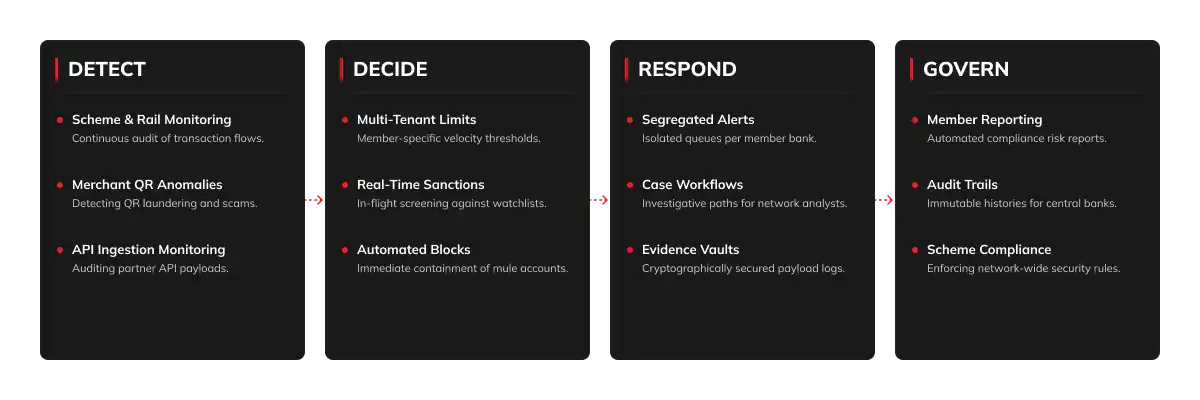

Managing network-wide fraud requires a modular control layer rather than a single monolithic platform. flxShield operates on this principle, isolating and protecting distinct clearing vectors through dedicated, interoperable modules. This modular structure allows switches to deploy targeted defenses where they are needed most. Learn more about flxShield for Networks & Switches and how it protects clearing ecosystems.

The platform orchestrates fraud mitigation through four operational stages:

Scheme Monitor provides scheme and network operators with a shared view of participant risk, monitoring clearing patterns from one common control layer.

Merchant Shield protects the merchant perimeter, analyzing post-onboarding patterns across the acquirer network to identify QR misuse, refund abuse, and transaction laundering.

Real-TimePay Guard secures high-speed, instant payment clearing streams, analyzing transaction metadata in parallel to flag transfers to suspected mule accounts.

Security Module | Target Attack Vectors | Technical Mechanism | Operational Benefit |

|---|---|---|---|

Scheme Monitor | Systemic clearing fraud, member bank terminal compromise | Rail-level anomaly detection, multi-participant pattern correlation | Identifies and contains coordinated network exploits before they scale. |

Merchant Shield | Transaction laundering, QR code scams, merchant refund abuse | Post-onboarding transaction profiling, velocity monitoring | Identifies fraudulent merchant networks across multiple acquirers. |

Real-TimePay Guard | Authorized Push Payment (APP) scams, money mule transfers | Parallel risk scoring, destination account velocity analysis | Flags high-risk payments in-flight before recipient accounts are credited. |

Shared Risk Operations with Multi-Tenant RiskOps

Establishing a shared security model across a national payment network requires balancing centralized risk coordination and individual member bank autonomy. Data privacy is paramount. Member banks must protect proprietary customer details and segregate operational workflows from competitors.

Operating a shared infrastructure through flxShield's Multi-Tenant RiskOps module resolves this operational conflict. The shared platform implements logical database partitioning, row-level security, and strict role-based access controls. This ensures that while the physical scoring infrastructure is shared, each member bank's customer data, alert queues, and case investigations remain strictly isolated and accessible only to authorized personnel from that specific institution. Centralized analyst teams can support member institutions, but alert queues, investigative workflows, and compliance reports remain operationally segregated.

This shared infrastructure model delivers distinct operational outcomes:

Optimized Technology Budgets Smaller member banks leverage the switch’s centralized scoring to defend against network-wide fraud (like coordinated money mule accounts) that requires cross-bank data. This helps smaller institutions avoid the compounding operational expenses highlighted in the LexisNexis True Cost of Fraud Study, which estimates that every dollar of direct fraud loss costs financial institutions more than three times that amount in recovery and operational overhead.

Aggregated Threat Intelligence Anomaly signatures detected at one endpoint are converted into shared threat indicators, allowing the network to flag matching behaviors across other member banks in real-time.

Enforced Compliance Standards The switch enables scheme operators to establish a uniform threat detection baseline, reducing the risk of a single weak link compromising the network.

Ecosystem Integrity: Watchlist Integrations and API Security

Securing national payment rails requires screening for international sanctions violations and third-party developer integration vulnerabilities in real-time. Threats require immediate interception. This checking must occur directly within the clearing flow without introducing processing latency.

Real-time sanctions screening scans originator and beneficiary details against global watchlists, PEP databases, and local registers. Running watchlist screening at the switch level acts as a network safety net rather than replacing member banks' legal compliance duties. While individual banks maintain final legal liability and KYC files, the switch screens transaction details in real-time. To meet latency budgets, the switch runs optimized, in-memory index matching against key sanctions databases in-flight, leaving complex fuzzy-name resolution to offline bank systems. Centralizing this screening ensures that updates are applied instantly across the entire network, flagging restricted actors that a member bank’s outdated database might miss, helping the network align with frameworks like the UAE Central Bank compliance standards and the Bank Indonesia retail payment regulations.

The expansion of open banking and BaaS models exposes the network to edge vulnerabilities where third-party fintechs connect to the ecosystem through sponsor banks and aggregators. While these integrations drive transaction depth, they create remote attack surfaces. Compromised third-party credentials allow automated bots to execute credential stuffing and micro-transaction validation testing through authorized endpoints. To counter this, the central switch deploys the API & Ecosystem Shield to monitor traffic behavior across sponsor bank connections, scoring inbound transaction requests for rate anomalies, credential abuse patterns, and payload mismatches that suggest a sponsor channel has been compromised.

Modernizing National Payment Infrastructure

Upgrading national payment networks to support digital trust is a strategic priority for switch operators. By transitioning from passive routers to active trust enablers, switches protect their ecosystems from systemic fraud, ensure regulatory compliance, and lower technology costs for member banks.

To support this shift, Filps provides flxShield. The platform is built from our global experience enabling payment networks across 60+ partner BFIs, managing security for 30 Million+ end customers served and 1M+ merchants with over $80 Billion+ in transaction volume, drawing from 21+ Years of institution-grade platform development.

Switch operators can begin this modernization through a phased approach:

Watchlist screening Run real-time sanctions screening hooks as a centralized safety net over clearing flows.

Multi-tenant risk engine Deploy centralized anomaly detection as a shared managed service for member banks.

API & Merchant Shield Monitor aggregator API connections and acquirer merchant networks for anomalies.

Transitioning a national payment switch from a simple message router to a shared trust provider is a critical modernization step. With flxShield, operators can begin this upgrade with a single module - protecting the most vulnerable clearing path—and expand as the payment scheme grows. Contact our team to book a strategy session or discuss a pilot scope for your network.